Q2 2021 Newsletter

To Our Clients,

Since I last wrote in April, we were in a transition process toward building a more robust practice, in order to meet the growing needs of clients and their families. Alison had gone on maternity leave and has since returned to her previous role as director of operations. During that time, Mike was wearing “two hats” and will now begin to work directly with clients on personalized financial plans using the award-winning software, MoneyGuide, which will help even the most complex goals and plans become a reality.

As I have spoken with clients during the preceding months a few have asked if plan on retiring soon and therefore, I would like to address that directly with everyone. I have no plans to retire in the foreseeable future. I can easily work another ten or fifteen years and have never been so fired up to grow the practice, as we now have the right people on our team necessary to deliver focused planning for each individual. Some may have even noticed we made a slight name change to reflect this new direction - Summit Investment Advisors. Our team believes it reflects the positive direction we are wanting to go with each and every one of you reading this newsletter.

The Pandemic Effect – Bottlenecks in Supply Chains and Record Market Prices

The first half of 2021 has come to a close, and the markets have continued a positive uptrend, with gains in most asset classes and individual equities. The Volatility Index (aka, “The Fear Gauge”) is hovering at its lowest levels since the beginning of the Pandemic. Yet, risks such as the Delta variant remain as its transmission rate increases through Europe, and it will likely become the dominant strain to affect Americans soon.

The market’s quarterly streak remains impressive. The S&P 500 hasn’t just gained for five quarters in a row. It has gained more than 5% for five quarters in a row, only the second time since 1945 that the index has been able to pull off that feat, according to Ben Levisohn of Barron’s Magazine.

Certainly, there will be sudden drops along the way. In 2018 and 2020, market declines continued for a few months. But, as Levisohn noted, longer-term investors are seeing signs that there is more potential for growth. Given all of the liquidity within the economy when measured using M2 (what the Federal Reserve uses to measure money in circulation) relative to GDP or the S&P 500, we can anticipate momentum being a dominant force for the markets in the near term as the increased money supply will be absorbed by various asset classes.

How Is Inflation Impacting the Economy and Markets?

Recently, Mike’s 7-year-old had asked him, “what’s inflation?” He told her that “it’s what you experience. It doesn’t matter what others tell you things cost. What does matter is what it costs you.” She then asked him to explain (she enjoys putting him through the wringer). He further explained that her Barbies are made by Mattel, which has recently warned investors that increased plastic costs will have to be passed onto consumers through higher prices at the register. Her new mountain bike has been marked up further due to a shortage in parts. The lower-end model was unavailable, and so we bought her the upgraded model as a result. Automobiles are no less immune, with new vehicle production sputtering due to a lack of CPUs and used car prices increasing as a result, which is factored into the Consumer Price Index (CPI).

Without a doubt, everyday consumers are witnessing inflation in the basket of goods and services they consume. From gasoline to groceries and even used cars and bikes, scarce commodities have driven the price surge in the preceding year. So much was the increase that new homes were costing buyers an additional $36,000 (on average) due to lumber shortages.

Yet, consumers haven’t been too concerned with rising prices, and the demand for goods and services will likely continue on a solid trajectory for the coming year. Consumer inflation expectations one year to five years from now remain somewhat subdued at 4% and 3%, respectively. Furthermore, many commodities futures are experiencing backwardation, which is when prices in the future are less than the current spot price. This has led to the Federal Reserve continuing with their current argument that inflation is actually transitory, despite our own misgivings with rising prices at the register.

This is directly impacting the markets with rising valuations of equities. Various market indices have reached historic highs. Many economists and financial experts have come to the consensus that the market has become relaxed because the Fed’s top management appears relaxed. If we were to look at the numbers on inflation, we would have doubts that it is transitory. However, as long as the Fed believes it’s transitory that is what matters for the markets. We have to listen to what the top Fed officials are saying even if we disagree with them in the short term.

We Cannot Control the Markets, But We Can Limit Risk

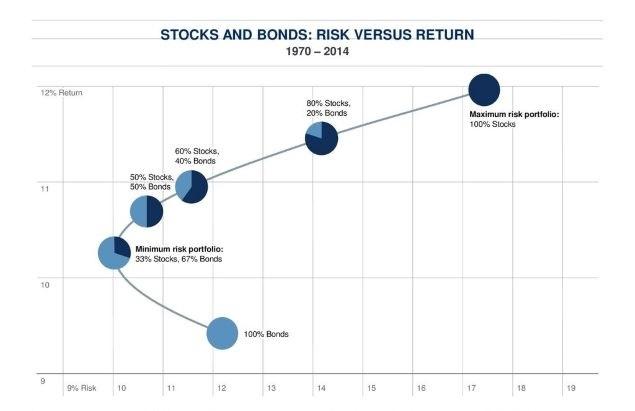

Even if inflation could be accurately forecasted, we do not know its effect on the stock and bond markets in the short to medium term. The adage, “don’t place all of your eggs in one basket,” holds with investment diversification as well. When we build diversified portfolios for clients, we reference The Efficient Frontier, which is a set of investment portfolios that are expected to provide the highest returns at a given level of risk, measured using volatility, or standard deviation.

The Efficient Frontier

The above chart references historical market performance of various investment allocations. What the data shows is enlightening as it answers the essential question, “for every unit of risk (volatility) what is my historical return?” As a client’s time horizon draws nearer to a goal, such as retirement, a portfolio should become more conservative by reducing risk while still maximizing return. However, it is vital to note what happens at the extremes with either 100% bonds or 100% equities.

A 100% bond portfolio actually assumes more risk than if we simply allocated a small percentage to equities such as a 10/90 or even a 20/80 portfolio. A 30/70 portfolio will also generate a much higher return compared with 100% in bonds while maintaining the same risk level. This 2.5% increase in average annualized return over the course of ten years on a $100,000 portfolio equates to an additional $32,430 in retirement. If we increase the time horizon or the investment amount, the results are even more drastic.

With regard to the other extreme, 100% equities assume excessive risk for such a small increase in annualized returns. In reality, many investors who hold such portfolios tend to buy high and sell low by allowing their emotions to dictate how they invest. Furthermore, rebalancing on a periodic basis prevents such a scenario from occurring by selling some assets that have increased in price (i.e, overbought) and purchasing others that have decreased (i.e., oversold).

Summing It All Up

Julia Carpenter of the Wall Street Journal put it best when she wrote that “good financial decisions are rarely made in the middle of an emotional maelstrom.” A common saying in the South is to “focus on the closest alligators to the boat.” The reality is we make sacrifices for our children and other family members and, yet we fail to do so for ourselves. Often, we explain to clients that “the most unselfish thing that one can do is become selfish for a change.” Like the emergency procedure when flying, we need to apply our own oxygen mask before assisting anyone else when it comes to our personal finances.

As we continue to grow the practice, we strive to provide holistic financial planning for every client. Proper planning with our team helps to provide a frame of reference to remain steadfast. While we often find ourselves discussing the financial markets, there is much more that begs our focus and that is always proper risk management to protect the ones we love as well as our income in retirement.

There is a great read by Jim Collins called ”Good to Great,” which I believe sums up well what we are wanting to achieve with Summit Investment Advisors. Those who build great organizations make sure they have the right people on the bus and the right people in the key seats before they figure out where to drive the bus. First, we had to find who those people would be and now we are wanting to deliver the what and how for every one of our clients.

As always, we welcome genuine conversations with clients and are humbled by your trust in referring others that see value in what we do to help families and friends achieve with their finances through proper planning.